Commonly held startup misconceptions I once believed

The world is full of common misconceptions. Did you know that:

- Napoleon wasn’t short. He was actually greater than average height for his time.

- Different tastes (sweet, sour, bitter, salty) can be detected on all parts of the tongue and not just in specific zones (maps of tongue taste zones are incorrect).

- Despite what multiple “science” teachers taught me growing up, blood in veins is not blue. Oxygen-rich blood is bright red while deoxygenated blood is dark red.

Startup land is full of misconceptions too. Working in venture capital for the last 5+ years I’ve had the privilege of speaking with ~1500 founding teams and have learned a lot about the beliefs of founders. Below are a few misconceptions I once held myself, that founders should watch out for.

Myth of the Lone Inventor

Calculus, the colour photograph, evolution, and even the lightbulb were each discovered independently by multiple people at the same time. This phenomenon, called multiple discovery, is well documented across a number of fields. More often than not, the myth of the lone inventor (or lone, genius startup founder) is a lie. Time and again we see smart, capable founders, unaware of each other’s existence, pitch the same business idea within months of each other and insist that they are the only ones working in that space.

Assume that other founders and incumbents are thinking about your problem space – even if you can’t find public information about them. Assuming they’re coming to similar conclusions, what will enable you to out-execute? What are your differentiated skills and insight?

Obvious Idea Bias

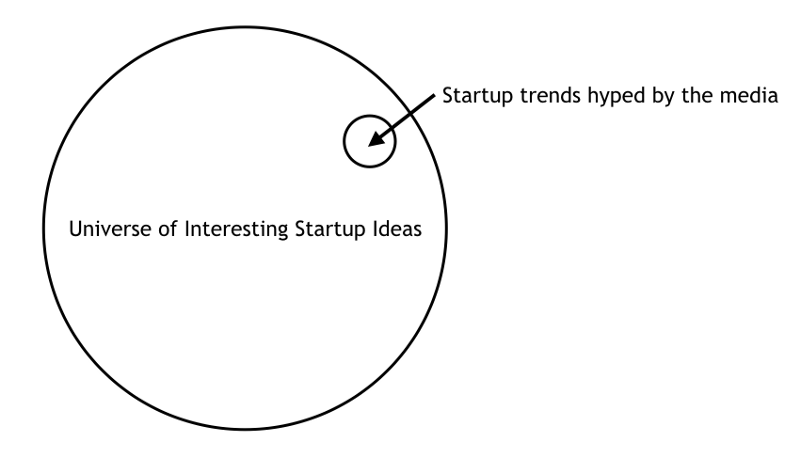

The startup world is notoriously trend driven. The hype around the connected home, drones, and consumer 3D printing has cooled and transitioned over the last few years into self-driving cars, industrial 3DP and scooter sharing. By the time a problem space is widely talked about, it has usually already reached a state of intense competition. Founders should have amazing reasons why the market needs another new entrant — yet most do not.

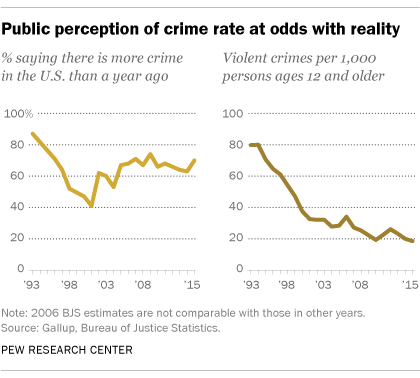

One reason for this may be due to the brain’s availability heuristic. This mental shortcut biases us to weight information more importantly if it’s easier to recall. A common example here is the persistent delusion that crime rates are rising in contrast to the persistent long-term drop in real violent crimes. Because the media reports violent crime so frequently, we feel that it’s much more important to be worried about than it is.

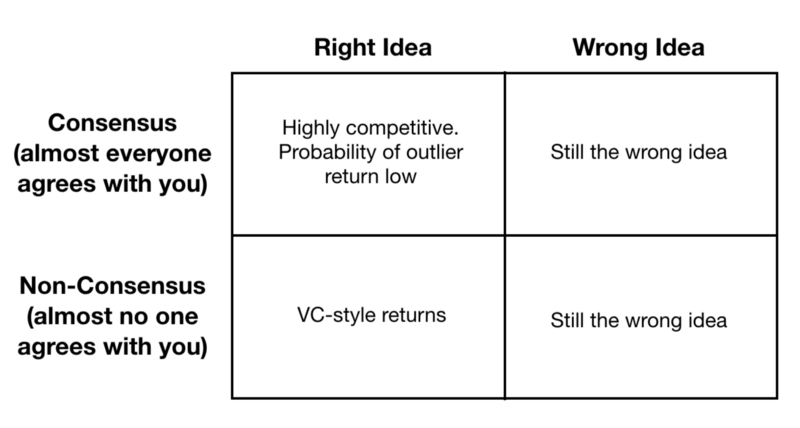

This same heuristic causes an over-abundance of founders and investors to work in problem spaces that are common, newsworthy and easily recalled to memory. Our subconscious tells us “Everyone is talking about 3DP so it must be a real opportunity”. There may be cognitive safety in numbers, but outlier value is driven by ideas that are both correct AND non-consensus.

Asked another way by Peter Thiel: “What important truth do very few people agree with you on?”. Choosing an idea that’s not already oversaturated is just as important as execution.

The Goal of a Pitch Deck is Not a Check

I used to misunderstand the goal of a pitch deck. Pitch decks don’t convince people to invest — they convince people to allocate time to you.

- The goal of an intro deck? Get a first meeting

- The goal of a full deck? Get a second or third meeting

Human connection matters. A key goal of pitch meetings is to evaluate the likelihood that a founder can convince others to work with them. To be successful, founders need to convince not just investors but an entire community of customers, employees, and service providers to join them on their journey. Decks are best viewed as visual aids that facilitate knowledge transfer and relationship building, not documents that unlock investment. The founders in our portfolio who have had the easiest time fundraising approach pitching as a human-connection-building process vs a rational, data-conveyance one.

Startup Competitions Are Not Reality

Over the last five years, I’ve observed a pattern with younger founders, particularly those fresh out of university. Many have solely worked in academic systems where next steps are prescribed: Finish this assignment → pass this test → complete this course → get a degree. They assume (I assumed!) that the startup world works the same way: make pitch deck → win startup competition → get into accelerator→ raise funding.

In reality, the entrepreneurial journey is more like a maze, with twists and turns caused by variables like competition, new technology, and customer feedback. It’s easy to get sidetracked down dead-end paths that seem like next steps and make you feel like you’re running a company but don’t actually increase your likelihood of success. Many competitions, conferences, accelerators, and crowdfunding campaigns are just distractions.

Avoid activities that aren’t directly related to achieving product-market fit and focus on gaining a better understanding of the core assumptions of your business model. Ask questions like: Do customers love my product? At what scale will we need to manufacture to be profitable? How can we scalably acquire customers?

Launch MVP ≠ Get Lots of Press

Similarly, most founders don’t realize that press and notoriety prior to shipping can be detrimental. Aside from the distraction, once news articles have been written there’s immense pressure to keep your company’s messaging the same. As humans, we want to appear consistent with our prior selves whenever possible. The trouble is, early-stage startups need to iterate significantly on product and brand.

Launching an MVP does not mean broadcasting what you’re working on to the entire world, it means getting your product in the hands of users as soon as possible. If you refrain from public-facing press, you’ll feel more enabled to iterate and won’t alert potential competitors to your presence. Traction is better demonstrated by a small group of highly enthusiastic users than 100 news articles or awards.

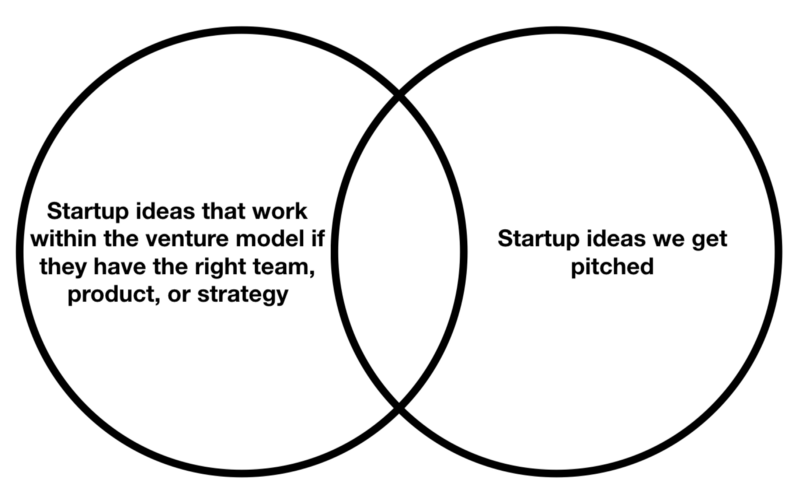

Misunderstanding Institutional Fund Models

It is entirely possible to identify a valuable market opportunity and assemble an “A” team but find it impossible to raise funding. This seems like an obvious point, but it’s not something I had internalized prior to working in VC. We consistently see founders pitching ideas that won’t have traction with institutional investors, no matter how good their pitch and product. Some market spaces just don’t have the right dynamics to make a fund model work — they’re either not large enough, not growing quickly enough, or not scalable enough.

Many paint this as greed, but it’s just how VC math works. When most early stage funds have loss rates of 40–70%, doubling or tripling a firm’s money doesn’t make a difference. They need 10x, 20x, or even 50x wins to make the fund model work. Venture firms are obsessed with $1B+ outcomes because their businesses won’t survive without them.

In markets that don’t have a high likelihood of venture-style outcomes, the hard truth for many founders is that they should have saved more money prior to starting, figured out how to ship on less outside capital, or chosen a different idea altogether. These are often not possibilities, especially for those who don’t start their business from a position of privilege, but understanding these dynamics prior to embarking on an entrepreneurial journey ensures founders go in eyes wide open.

Bolt invests at the intersection of the digital and physical world.